Worried that markets look uncertain? Remember these 3 simple rules

Inflation, high interest rates, financial markets moving up and down. In this sort of environment, it’s tempting to hit the panic button. When you’re looking for reassurance you’re doing the right thing, there are three golden rules to hold onto.... Read more

Inflation, high interest rates, financial markets moving up and down. In this sort of environment, it’s tempting to hit the panic button. When you’re looking for reassurance you’re doing the right thing, there are three golden rules to hold onto.

Rule 1: ‘The good things outweigh the bad’

When stock markets are as volatile as they’ve been in the last year or so, it’s natural for anyone but the most seasoned investor to get nervous.

But watching the day-to-day movements of a market, currency, or a company’s share price are a distraction – they can spring back up as quickly as they fall. It’s always better to ignore the short-term noise and view things with the benefit of some longer-term perspective.

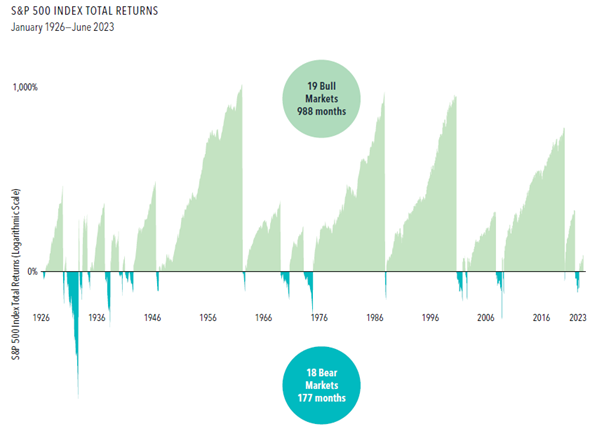

The chart below (Chart 1) gives about 100 years of this perspective. The reassuring message behind it is that, more often than not, the good things outweigh the bad.

Investors talk in terms of ‘bull markets’ and ‘bear markets’. The bull when stocks rise and keep rising, the bear when they continue to fall.[1] As we can see, since the 1920s, there have been some notable bear markets, taking in some high-profile occasions where global stock markets have blown up: the Wall Street Crash in 1929, Black Monday in 1987, the dot.com boom and bust in the late 1990s and the 2007/08 global financial crisis.

But, over time, the bulls tend to outnumber the bears. Not only that, but the up periods last longer, and the highs are much greater than the lows. For the example below, the S&P500 saw 18 bear markets, averaging 10 months long, and falls of up to 80%. By comparison, there were 19 bull markets. But these lasted considerably longer (averaging 52 months long) and had much higher peaks (rising as much as 936%).[2] While this chart only focuses on US stocks, it’s a trend that is also evident in UK and global markets.

Chart 1 Bulls last longer than Bears

Source: Dimensional. Past performance does not guarantee future returns. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio.

Rule 2: ‘No one can predict the future’

We’ve written a lot about high inflation and rising interest rates over the last couple of years. We know it’s something that worries clients as they think about how this could impact their long-term financial goals.

We even get asked by some clients if they should move their money temporarily into cash (rising interest rates might be bad news for mortgage holders, but they have pushed up savings accounts to 6% or more). In theory, one could dip in and out of the market, avoiding the biggest drops and gaining maximum benefit when share prices begin to surge once more.

Except…

No one can predict exactly where those inflection points between bear and bull market will come. And missing the market’s worst, often means also missing out on its best. As Chart 2 shows, a hypothetical investment in the Russell 3000 index from 1998 to 2022 could have turned US$1,000 into more than US$6,000.

But missing the best week (in November 2008, as the global financial crisis rolled on), cuts the final investment pot by around US$1,000. Missing the best six months, would have meant losing out on more than US$2,000.[3]

What does this tell us? Trying to ‘time the market’ is at best a risky move. At worst, it could be potentially catastrophic.

Chart 2 Avoiding the market’s worst days may mean missing its best as well

Source: Dimensional. Past performance does not guarantee future returns. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. In USD. For illustrative purposes. Best performance dates represent end of period (November 28, 2008, for best week; April 22, 2020, for best month; June 22, 2020, for best three months; and September 4, 2009, for best six months). The missed best consecutive days examples assume that the hypothetical portfolio fully divested its holdings at the end of the day before the missed best consecutive days, held cash for the missed best consecutive days, and reinvested the entire portfolio in the Russell 3000 Index at the end of the missed best consecutive days. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes.

Rule 3: Stick to a plan

So, what’s the final golden rule?

Whatever you want to achieve financially, whether it’s a comfortable retirement, or leaving a legacy, a plan is vital.

And like the other two rules we’ve featured here, it’s important to follow the evidence.

At AAB Wealth, we take a rigorous, evidence-based approach to help make the best financial plan for you.

We use cashflow modelling to explore the impact of events or lifestyle choices. This helps you answer those all-important questions such as “Can I retire early?”, “Is my wealth protected?”, and “How do I make sure I leave something for my loved ones while still enjoying my retirement?”

The plan isn’t rigid. It adapts when necessary, depending on changes to your personal circumstances, your financial objectives and sometimes the economic environment, but it allows you to look past the short-term ups and downs, to concentrate only on the long-term health of your finances.

First, we get a clearer picture of what’s most important to you – including any goals you have on your ‘bucket list’. Then, we analyse your current arrangements in more detail, so we can recommend an appropriate investment plan and advise on tax-efficient succession planning. Once you’re on board, we review your goals and objectives regularly, including an annual progress meeting.

Uncertainty is a fact of life, but with longer-term perspective it can look a lot less daunting. Remembering these three rules can help ease the pressure and take some of the sting out of saving.

Don’t believe the hype: those predictions you’ve read are probably wrong Stock market forecasts at the beginning of each year make interesting reading – but we shouldn’t always expect them to get it right. In fact, pay too much attention... Read more

Why the headlines aren’t always as bad as they seem

There are plenty of scary headlines doing the rounds about pensions and markets at the moment. And it’s led to a lot of nervous questions from worried investors. The mini budget at the end of September didn’t help. It sent... Read more

Returning to AAB Wealth – from Aberdeen to Belfast

In January 2021, Alastair shared an update on how things had changed in his career after achieving his advanced diploma in financial planning. Since then, Alastair has been busy, in fact he left AAB Wealth in November last year to... Read more