Elections don’t have to spell panic for your portfolio

Is a Labour or Conservative government better for my investment portfolio? Will markets crash if Donald Trump gets into the White House? 2024 is a year of big elections, but they might not have the impact that you think. This... Read more

Is a Labour or Conservative government better for my investment portfolio? Will markets crash if Donald Trump gets into the White House? 2024 is a year of big elections, but they might not have the impact that you think.

This year will see a record-breaking number of elections worldwide. Around 2 billion people are voting across 64 countries. Among them, a rematch between Donald Trump and Joe Biden for the US presidency, and in the UK, a Tory party hoping to hold off a serious challenge from Labour, after 14 years in charge.

Investors don’t tend to like big changes or surprises, so election time can be quite a nervy affair. In the last few months, we’ve had a number of questions from clients about how this year could affect them. Will Trump ‘Mark 2’ be good or bad for markets? Will a Labour victory mean higher taxes?

The good news is that with the benefit of prudent long-term financial planning, things needn’t change much for you at all.

How politics impacts your portfolio

There’s no denying the influence politics can have on markets. A change of policy, new regulation, or a tax increase can push share prices up or down.

Sometimes a single event has an instant and dramatic effect (just look at what happened after the Liz Truss mini-budget in 2022). But, when viewed through a more long-term lens, things don’t just fall off a cliff. The big losses are only temporary.

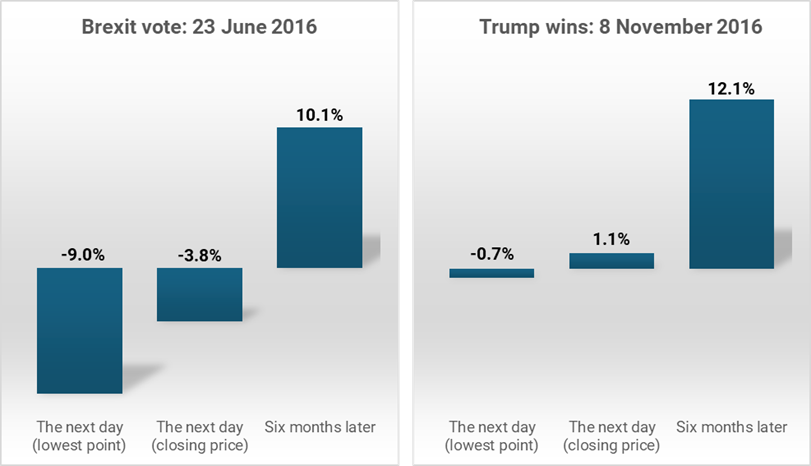

To illustrate this point, let’s look back to 2016 – a year of two serious political shocks. The UK voted to leave the European Union, and Donald Trump defeated Hillary Clinton in the US. Both events went against poll predictions. Initially, both caused a stir in investment markets.

The UK market fell in the immediate aftermath of the Brexit vote on 23 June (as the chart shows, the FTSE All Share was down 9% down the following day at its lowest point). Six months on though and the market had recovered. Global markets also fell in the November when it became clear Trump was likely to win but the slump didn’t last long. In fact, the US market actually ended the day after the election slightly up.

Of course, these are just snapshots, but they illustrate a wider point that markets tend to shrug off elections, even the really surprising ones. Looking long term, the volatility evens itself out. So, when voters go to the polls, there’s no need to panic.

Source: Investing.com, Chart shows performance change between the day before the Brexit vote (23 June 2016) and Trump’s election victory (8 November 2016) and the lowest point in the market the day after, the end of the next day and six months on. UK market data is FTSE All Share (in sterling), US market data is S&P 500 (in US dollars).

Planning not panic

Of course, with wall-to-wall election coverage, dialling down this panic can be difficult. This is where good financial planning becomes so important.

Our role at AAB Wealth is about making sure we get the details right. That means making the most of any tax advantages available at the time (such as ensuring you’ve used your full ISA and pension allowances), ensuring your plan is always aligned to your goals, and checking in with you to ensure the strategy is up-to-date.

These details may seem small at the time, but they make a huge difference. And they mean we’re always prepared for potential surprises.

Additionally, as part of the wider AAB Group, you benefit from expert financial planning and tax advice all under one roof. This comprehensive approach helps us to create a truly in-depth plan that can withstand any short-term shockwaves.

When you speak to us, our Chartered Financial Planners create a detailed personalised lifetime cashflow forecast. They then stress test it in different scenarios, considering outside influences such as rising interest rates, or the impact of changing personal circumstances.

At the same time, our tax experts explore in greater detail areas such as reducing your tax liabilities (including inheritance tax and capital gains) to help you get the maximum out of whatever assets or investments you have.

A final thought

Imagine a big rugby match, the final weekend of the Six Nations at Murrayfield. The coach has carefully worked out a game plan to take on the opposition, with carefully judged tactics on how to approach every line out, maul and scrum.

But as game day approaches, the weather forecast changes. Instead of a calm, sunny day, it’s now looking like wind from the east. Does this mean throwing out the whole play book and starting again?

Quite simply, no. It’s just one of 101+ variables that have already been prepped for. A successful coach takes the new information, makes small adjustments where necessary and adapts the game plan. It’s very similar to our approach to planning – no single event will ever undo the strategy we’ve carefully created.

Speak to us about how our services can help you create a plan that withstands short-term shocks and gives you confidence in your portfolio.

How a financial planner can support you through divorce

Divorce means unravelling years of shared finances while you’re processing profound emotional loss – and making sound decisions during this time can feel overwhelming. A financial planner offers calm, impartial support through this transition, helping you protect your long-term security... Read more

Three scenarios where financial planning can make a big difference

Financial advice isn’t just for those about to retire. Whatever stage of life you’re at, you can benefit from greater clarity on the road ahead. Here are three scenarios that show how financial planning can help you no matter where... Read more

If you own a family business don’t forget these 5 important rules

Family businesses are the lifeblood of the UK economy. Working alongside your partner or children can be rewarding and even bring tax advantages. But running one is a delicate balancing act, with emotional ties that sometimes prove complex to unravel.... Read more

Important changes to your National Insurance contributions

AAB Wealth would like to make you aware of an upcoming change to the rules concerning the purchasing of voluntary National Insurance contributions. A person typically requires 35 full years of National Insurance contributions to be entitled to a full... Read more