Two important lessons we can learn from the ‘everything rally’

Market commentators feared the worst for 2023. But despite global uncertainty, the predicted slump turned into the ‘everything rally’ – a surprising surge taking in stock and bond markets. Here are two things it can teach us when it comes... Read more

Market commentators feared the worst for 2023. But despite global uncertainty, the predicted slump turned into the ‘everything rally’ – a surprising surge taking in stock and bond markets. Here are two things it can teach us when it comes to our own investments:

Lesson 1: Never mind appearances, cash isn’t king

As markets went up and down last year, some clients got in touch to ask about cash rates.

The big question: “Why should I risk losing everything on the stock market, when I can put it in a high-yield cash account instead?”

They weren’t alone. Global investors put a record US$1.3 trillion into cash over the course of last year[1].

But as we discussed back in July, when higher cash rates were turning some investors’ heads, this is not always the great deal it appears to be. Even though current deals are still much improved on previous years (with up to 5.15% for easy access or 5.16% for a fixed-rate account), our advice is the same: cash isn’t king.

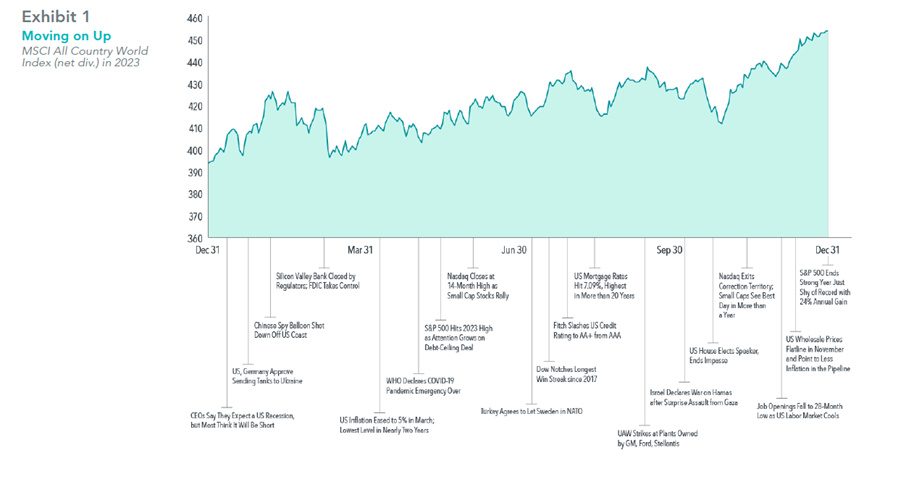

Take 2023 as a whole and markets bounced back. The S&P 500 (the largest companies in the US) rose just over 19%, and the MSCI All Country World Index (which includes companies from both developed and emerging markets), rose 15.3%.[2] Bond markets were also up, with short-dated bonds recouping more than half their 2022 losses. Other assets, such as property and infrastructure also made gains. At around the 5% mark, cash was up, but couldn’t match the pace elsewhere.

There’s a popular phrase in investing. “Time in the market is better than timing the market”. Switching to cash to cut your risk would’ve missed this rally, and would also have meant losing out on the compounding effect from remaining invested. Investors who stay disciplined on the other hand, will be rewarded.

Lesson 2: Home isn’t always where the heart is

So what about UK stocks? They also rose in 2023, but didn’t have anything like the standout year experienced elsewhere. That brings us onto the second lesson from 2023: avoid home bias.

When we send out monthly market commentaries, clients often ask us why we focus so much on what’s going on elsewhere, particularly the US – why should a UK investor be worried about what the US Federal Reserve is doing?

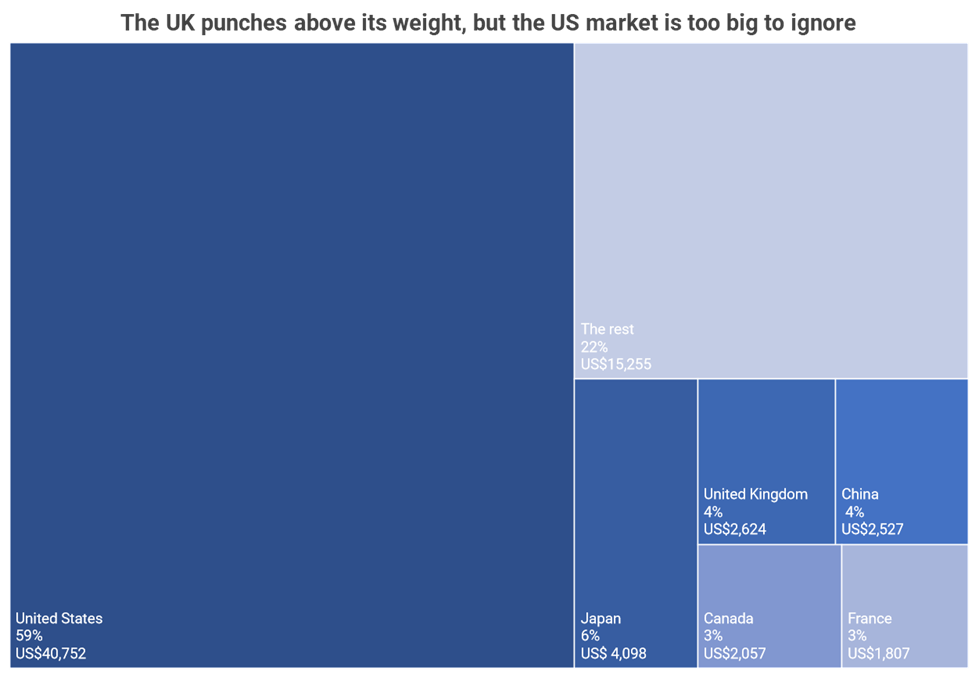

The reality is, in global terms, the UK really isn’t that big. With 595 listed companies, UK equities make up around 4% of the world’s market cap. If it was a company, it would slightly bigger than Apple (but not much).[3] By comparison, US stocks account for around 59%. That’s a market just too big to ignore.

True, the UK still punches above its weight (apart from the US, only Japan’s market cap is bigger). But its relevance to the bigger picture is often minimal.

Source: Dimensional Matrix Book 2023. Percentage of market cap. Market cap (US dollars) in billions.

But it’s not just about size. Being too focused on your home market means missing out on potentially key sectors.

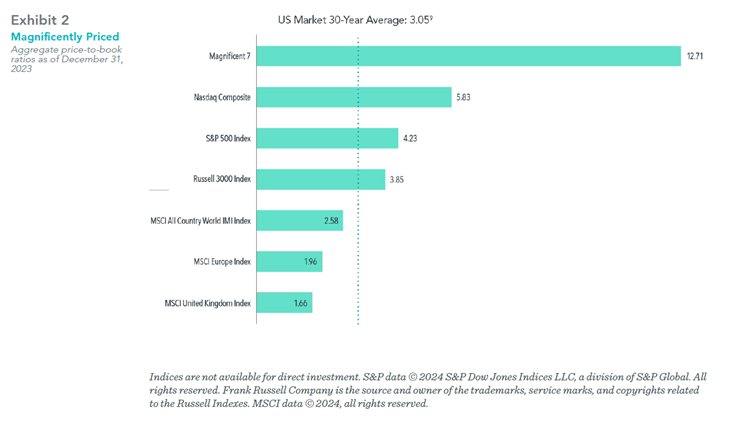

The 2023 rally was a case in point. One of the main drivers was investors getting excited about technology, especially the rapid development of artificial intelligence (AI). The biggest market movers were the seven US tech giants (or, at least, tech-related), now dubbed The Magnificent 7, who are leading the way in this field: chip designer NVIDIA, Microsoft (the largest investor in AI game-changer Chat GPT), Google’s owner Alphabet, Amazon, Apple, Meta (Facebook’s owner) and Tesla.

Combined valuations of Magnificent 7 greatly outweigh those of other markets

When there’s a tech rally, the UK gets left behind. Technology makes up only a small fraction of UK indices. So, while the Magnificent 7 dominates the S&P 500, a glance at the top of the FTSE 100 has a very different feel, featuring oil companies, pharmaceuticals, banks, and consumer staples.

S&P 500 Top 5

FTSE 100 Top 5

Apple

Shell

Microsoft

AstraZeneca

Amazon

HSBC

Nvidia

Unilever

Alphabet (Google)*

BP

By index weight. Source S&P Dow Jones and FTSE Russell as at 29 December 2023. Alphabet is listed twice in the top 10 as it has two listed share classes.

Home bias – disproportionately allocating domestic stocks in your portfolio compared with their share of the global market – can have a damaging effect on long-term performance. By one estimate, UK investor portfolios contain around five times the allocation of domestic stocks than the UK’s market capitalisation.[4] Analysis from Barclays, comparing different levels of UK home bias against a world benchmark, showed that the greater a portfolio’s home bias, the greater the risk for the investor relative to the benchmark. Portfolios with a lower home bias had a greater investment return.[5]

So while there’s a temptation to stick with what seems familiar and favour UK stocks this isn’t always the best route for long-term investment success.

One last thing: diversification is key.

Of course, no rally can be sustained indefinitely. Even as 2024 began, there were already signs the ‘everything rally’ was petering out. Also, while the high valuations for the Magnificent Seven shown in the chart look impressive, many will be wondering how long until some kind of correction.

But with the two lessons from last year in mind, there’s something else that investors need to remember: diversification.

Particularly with so much noise around markets, it’s vital to maintain a spread of assets, sectors, and regions, to ensure that you’re able to benefit from positive news, but give your portfolio protection whenever there’s a dip.

The key to do this, we believe, is adopting a rigorous, systematic, evidence-based approach. By staying disciplined and diversified we can avoid the need for making impulsive – and expensive – investment decisions.

[2] Source: Dimensional. Data for S&P 500 and MSCI indices based on returns from Dec. 30, 2022, to Dec. 29, 2023.

[3] Source: Dimensional Matrix Book 2023. As of 31 December 2022.In US dollars. Market cap data is free-float adjusted and meets minimum liquidity and listing requirements.

[5] Barclays Private Bank Overcoming home bias when investing Comparing hypothetical risk-adjusted returns of equity portfolios using the MSCI All Countries World Index ex UK and FTSE 100 between 1999 and 2023.

It’s summer! A chance to let your hair down and savour the moment. But is your financial plan flexible enough to do this? Can you enjoy ‘now’ or are you holding too much back for the future? What event would... Read more

It’s summer holiday time. How to make the most of ‘now’

Financial planning shouldn’t just prepare you for the distant future, it should also help you to enjoy the special moments that come along the way. Holidays don’t come cheap… This summer, UK holidaymakers are steeling themselves for costlier trips abroad.... Read more

Asking these 5 big questions? You need a financial planner

Seeking advice isn’t just for the super-rich. And it’s not just selling you investment products. If you’ve never talked to a financial planner, you may be unaware of what we do and the important questions we can help you answer.... Read more