Whatever your investment experience, deciding to go it alone with no external support can be a risky move. One investor’s decision to “wait and see” during market turbulence earlier this year actually cost them £51,000 in missed gains. Beware the... Read more

Whatever your investment experience, deciding to go it alone with no external support can be a risky move. One investor’s decision to “wait and see” during market turbulence earlier this year actually cost them £51,000 in missed gains.

Beware the pitfalls of DIY investing

The number of ‘self-directed’ investors is on the rise. In recent years, more people have opted for the DIY investing route instead of seeking professional advice. By some counts, as little as 9% of the UK population received paid-for financial advice in the last two years.[1]

For some, the motivation is cost or not feeling they have the assets that justify speaking to an adviser. For others, there’s a feeling they don’t need to involve an outsider. One in four surveyed this year said their reason for not taking advice was “I can look after my own money”. [2]

But there can be a hidden cost to not taking professional financial advice. Without impartial, expert guidance, investors risk making emotional mistakes that could harm their long-term returns.

The costly mistakes even experienced investors make

One of the biggest investor errors is making decisions in the heat of the moment. Even those who consider themselves fairly well informed on investment topics (even those who work in the financial sector) will sometimes get nervous when the market starts to fall. Without external guidance, it becomes much harder to avoid being reactive at the expense of long-term planning, because we’re all often easily swept up in emotions.

These emotional errors can often be compounded by others: for example, failing to sufficiently diversify your assets; showing bias toward stocks you feel familiar with; or missing your own investing blind spots. Many investors are guilty of following the herd on particular trends, or only listening to good news (or bad news) on a theme rather than considering all available information.

These errors can end up costing you dearly over time. Whereas a financial adviser can act as your objective counterweight to these natural tendencies – providing the diversification expertise you might lack, challenging your familiar stock preferences, and most importantly, offering an impartial perspective when emotions are running high. Where DIY investors often react, advisers help you respond strategically.

Here’s an example where not taking advice had a hidden cost

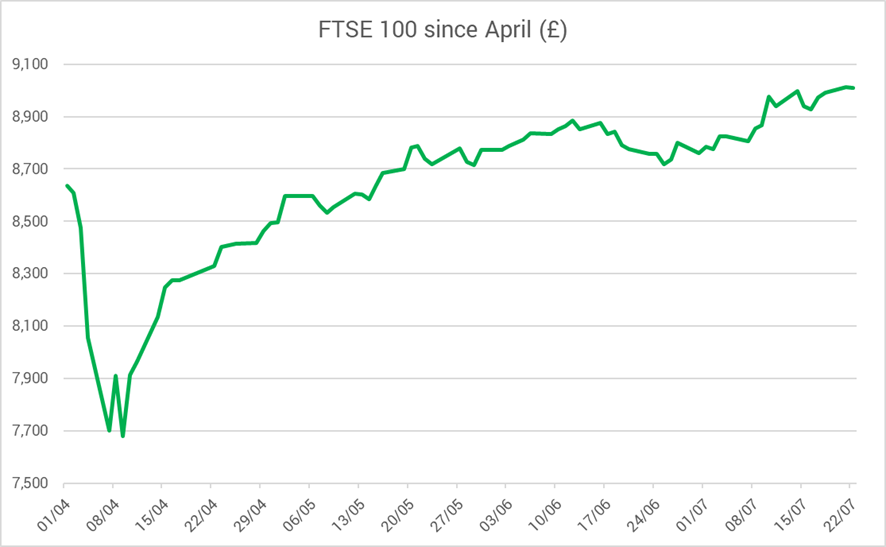

Was this an investment gain or a lost opportunity? Back in April, with markets in turmoil following Donald Trump’s ‘liberation day’ tariffs, an investor has a windfall of £400,000 but decides to only invest £100,000 of it, holding back on the rest until the market recovers.

Fast forward to mid-July and markets have shrugged off the uncertainty. The FTSE 100 has broken the 9,000 barrier for the first time and risen more than 17% from its low point.

The good news was that their investment has grown to around £117,000 – a healthy return that would seem like a resounding success. To the DIY investor this might seem like a win. But here’s the hidden cost: if they’d invested the full £400,000, their gains would have been around £68,000 instead of £17,000. That’s a £51,000 opportunity cost for trying to ‘time the market’.

Our advice at the time would have been that holding capital back in this way would potentially do more harm than good. That’s because timing the market rarely works – partly because it risks missing the best days in the market; as we explain in our article here, even just missing a few can dramatically reduce your returns.

For us, that gap – the difference between actual investment growth and what might have been – is the hidden cost of not taking advice and shows the value of talking to a financial planner.

What a financial planner can do for you

Our role is providing the insight and perspective that helps guide you forward. Here are three key benefits of working with us:

1. We’ve seen this before

No one can predict the future and past performance doesn’t equal future returns – but we can look at history. While the 17% recovery in our example happened unusually quickly, it demonstrates a pattern repeated throughout history. With a balanced portfolio, diversified among sectors and asset types, staying the course typically pays off. This chart from Dimensional shows that one dollar invested in global markets (MSCI World) at the beginning of the 1970s would be worth US$126 today.

2. Keeping a cool head when it matters most

Saying “stay the course” is one thing. Actually doing it is quite another. That’s where an impartial adviser proves invaluable. We can take a cool-headed look at your portfolio and make rational assessments based on data, rebalancing when the time calls for it, but also knowing when no action is the right action.

3. Planning beyond the headlines

This isn’t just about hoping for the best. As financial planners, we help show you the potential consequences of your actions and the different scenarios your plan might take in the future. We use cashflow modelling to demonstrate how various decisions could impact your long-term financial goals – giving you clarity that goes far beyond today’s market movements.

You remain in control

When you work with us as financial planners, you’ll receive expert guidance, but the final decision is always yours. At AAB Wealth, we set out the options available to you, but there’s never any pressure to follow our recommendations.

Research from Boring Money found that of those who are taking advice, 96% reported net satisfaction and 79% were extremely or very satisfied – evidence that advisers are delivering real value.

Professional advice isn’t just about avoiding costly mistakes – it’s about having the confidence to make informed decisions that align with your long-term goals.

If you’re interested in how a financial planner could help guide you toward the best options for your finances, please get in touch.

What’s the best way to pass on your wealth? When does a good deed become a burden? With Christmas being the season of giving, we’ve taken a look at some of the most important things to remember when it comes... Read more

The LTA is no more: what does that mean for your pension death benefits?

The UK government has scrapped the lifetime limit on what you can pay into your pension. But what happens next? If you’re leaving your pension to someone after you die, here are some important questions we’ve been helping clients answer.... Read more

How Accountants and Financial Planners Team Up for Success

When you work with a financial planner, the last thing you want to hear when asking for tax advice are the words: “That’s outside my area of expertise”. Some financial planners are in a position to offer some tax advisory... Read more

What the Magnificent Seven can teach us about hindsight in investing

The seven biggest US technology giants, known as the Magnificent Seven, completely dominate global markets. While it might seem now as if their time at the top will go on and on, it’s important to remember that nothing lasts forever.... Read more